| The basic

difference between LCA and SEA (figure from the SEA research paper wind farm example) |

|

) |

For LCA -

a 1/5 slice Counted |

The Oil Man helps explain the "reality math"

Whole Systems Energy Assessment - SEA

|

The basic story: There's been a long standing scientific problem with how sustainability metrics have been defined. We've been doing sustainability assessments by “counting up” what businesses can trace rather than “dividing up” between businesses what the economy is responsible for, to assure full accountability.. The latter approach can capture 2 to 10 times the impacts compared to what the still standard approach finds to count. It becomes a difference is what categories you count. The standard methods count the traceable material supply chain impacts, and SEA counts the economic demands for services created by what the business pays for to operate. An environmental impact is a very diffuse global effect, something every business contributes to globally with all its materials and services chains, with both employee and technology impacts of great variety, literally scattered around the world. Without lifting a pen you can be sure that "on average", every business will be responsible for a share of the world economy's impacts proportional to its share of the world economy. So, an accurate accounting of material impact responsibility and risk exposure needs to be for a business's share of the whole economy's impacts, not just a list of the impacts you can find to count. It can first be calculated as if "just to check the math", and compare the total impacts the business is able to count, and it's implied share of the economy's total. That's how physical science measures are designed, with defined units that are defined fractions of a scale. Using that approach results in a far more accurate accounting, and so a huge shock when you look at the numbers. The 2011 paper was in the online journal Sustainability, and as a local PDF. In 2014 a generalized version was developed for discussion at the UN's meetings on Post2015 Sustainable Development Goal, called A World SDG, as a practical system for "internalizing all direct externalities". It would, conceptually, assure fair global accountability for the impacts of all kinds of economic choices, by businesses, consumers, investors and policy makers. |

|

SEA provides a general method for: |

The World SDG then

It would help inform decision makers on true relative benefits and harms of their choices, and so improve long range investment and policy choices. |

| The basic

difference between LCA and SEA (figure from the SEA research paper wind farm example) |

|

|

|

For LCA -

a 1/5 slice Counted |

The Oil Man helps explain the "reality math"

__________________

Recent related RNS Journal posts:

Easy Intro, “scope 4″ use & interpretation,

What’s “Scope 4″, and… Why all the tiers??,

How full is a “Glass Half Hidden”?

A World View of Off-Shore Energy use,

A telling image… Money Measures our Impact

|

Published in Sustainability (MDPI)

Oct 2011

in a Special Issue New

Studies in EROI (Energy Return on Investment

edited by Charlie Hall.

Pre-publication copies of the paper are

deposited in the Cornell physics archive

arXiv:1104.3570v1

and local PDF available

on Synapse9 as

System

Energy Assessment (SEA)

Preliminary Paper Awarded ASME "Best energy paper of the year", for the May 2010 ASME-ES Meeting as EROI for Wind farms - whole system 'Bottom-up' and 'Top-down' Accounting methods then same content expanded for Sustainability Published review article in Sustainable Brands as Shining Light on “Dark Energy": the total impacts of Business in Nov 2012 "New Metrics of Sustainability" collection. |

________________

Related Links - Other Reality Math links - Notes - Slides

Short Discussions below:

Basic findings

Why impacts measured without known uncertainty hide large

errors that are highly misleading

The historical accident -

What

difference it makes

________________

|

The standard measures of business energy use, like LCA, count energy uses paid for as costs of employing technology in business operations, but do not count the energy needs of the self-managing services businesses need to employ too. A business's self-managing services don't record or report their energy use, so a choice to count only reported energy use is a decision to omit the great majority that go unreported. Those include the energy uses paid for as a cost of employing labor, management, design, advertising, maintenance, Insurance, finance, rent and taxes, etc, all of which generate "consumption for production" costs as necessities of operating a business. A method of combining the reported and unreported energy demands is needed to get an accurate total. The systems physics needed may be the more important finding in the end. To decide what "unreported" energy uses to count it relies on identifying the natural physical boundary of a whole working unit of the economic environment. It may be the first attempt to objectively fit a scientific measure to the natural physical boundary of a whole distributed net-energy system, a natural unit of environmental organization that grows and behaves as one. Identifying "a business" as a working unit of organization in nature, (as a self-defining object) departs from treating it as a theory of equations representing recorded data . That creates a whole new subject for physics, as well as for economics. Environmental systems become physically accountable net-energy systems, as having a natural boundary and subject to traditional thermodynamic analysis. So it allows them to be studied in their organic form, rather than as theoretical models missing unknown amounts of the energy information needed to close the equations. |

|

|

|

|

(from the SEA study of a typical industrial business, a wind farm in Texas- Slide 2)

|

|

|

The difference is whether households and businesses work independently or as combined units |

|

|

|

|

|

3. describing environmental impacts of business using standard business financial accounting categories, and so identifying only the plant and equipment, and their consumption for production |

4. describing environmental impacts of business according to the naturally defined working unit, composed of all the parts that physically work together, and their consumption for production |

|

|

|

|

|

|

Why impact measures lacking

measures of uncertainty, There's been a longstanding quandary in sustainability science about how to count the untraceable direct impacts on the environmental of business operations. The consensus was to ignore them, as it could seem the were counted in someone else's impact budget as traceable impacts. the of course hugely biases the decision making of a business to be unaware of the scale of its purchased "outsourced" impacts that the world accounting method assigns to someone else... So, for the measures of individual impacts the problem of how to estimate the impacts of its purchases of services that go uncounted has just been ignored, appearing to be a necessity. Unaware that ignoring the individually untraceable portion of business impacts would make impact measures scientifically indefinable, and so not valid as physical measures. What it's been hiding are errors in impact estimates on the scale of 80% or more (basic findings). I’m the systems scientist who got to the bottom of it, starting with a way to give environmental impact measures a well-defined uncertainty, and demonstrating a practical method using currently available data to generally apply it to sustainable design problems. In the figure below, to use impact measures accurately to compare "before & after" for example, and also be sure of accounting for the Observed world of impacts 'A' , an accounting estimate for the Likely total as a share of the world total 'B' needs to be compared with the Traceable impacts total 'C'.

Without a way to estimate the untraceable part of the impacts attributable to a business that creates the demand for them by employing them to operate, enormous errors are made, often to "outsource" more and more impacts that won't get counted... thinking of it as a sustainability plan. Using the small directly traceable part is simply invalid as an indicator of the total. If the numbers aren't right the decisions won't be For sustainability our requirement is to “work with nature”, not to mismeasure nature to improve "the bottom line" using ill-defined measures. It’s really long past time to talk about how to define our units of measure, and the scientific implications. More accurate and truthful measures both greatly simplify some parts of the larger problem, and change some of the terms of discussion… (with what is also an extremely cool bit of useful hard science) pointing us in the right direction. ___________ Other scientific principles for connecting numbers to reality are in the sections 1.2, 4.1, 2, 3 & 4 and 5 in the paper. Here are three:

It's highly valuable to find dangerous mistakes that are correctible. 6/26/13 6/27 |

| The Estimate methods, models & examples |

Reading Nature's Signals, Blog Articles |

|

An accident of history resulted in way resources consumed by machines are measured, an efficiency measure, to become our standard way of measuring the environmental impacts of business. That leaves out the consumption of the people that run or serve a business, such as by operating the machines. Economists were accounting for paying people or purchasing services only as an exchange of money, as if decoupled from what the money was used for. How the energy used by businesses has been counted is by just adding up the traceable energy uses of business technology. That overlooks the energy uses throughout the economy consumed in delivering business services. A statistical method is needed, because they are spread throughout the economy, paying people on the long chains of services needed by business. Those chains all end in paying some person for their normal consumption, as the end users of the business payments, made for their part in delivering the end service a business needs and pays for. That exposes a giant "technical definition error", of confusing economic measures and environmental measures. That's what SEA discusses and provides a fully rigorous physical systems science approach to correcting. The new approach to environmental impact accounting is both far more accurate and much easier. The useful conceptual finding is that the services delivered by any dollar, or in the used of any dollar, are widespread throughout the whole world economy, making the use of any dollar need to be first assumed responsible for an equal share of the whole world economy's impacts. So... taking a Texas wind farm as an example, the SEA study then shows that commonly 80% of the energy use and its environmental impacts go uncounted in environmental impact measures using the LCA method. Trusting a measure of technology efficiency, commonly accounting for only 20% of the total, has then resulted in major conceptual errors in the design of models for making businesses sustainable on earth. The real challenge is that the "reality math" says:

the

default (not ideal) path to sustainability is

shrinking the economy without lasting loss of human welfare, and

*not* to make expansion of the

economy

|

|

Good models for explaining it in a short letter:

1) To ClimateCoLab - 5/23/11 idea of quantifying local effects and impacts and Original Thread with this comment

The one I'd recommend, for how individuals can understand their own energy and CO2 footprints, would also help you clearly understand what is and is not meant by "zero carbon" or "zero net-energy" claims. That's my new resource page (still in development), for just that. www.synapse9.com/pub/SEA

A new method of doing global energy accounting simplifying things a lot, actually, from having to correct a very major omission in the standard accounting method for environmental energy accounting. Businesses now count up all the fuel purchases they make, and add the fuel purchases of their *producer product* businesses in their supply chain. They have NOT been counting the energy uses they pay for as a cost of business for the businesses offering *producer services* in their supply chain, only those for producer products.

So... that results in under-counting the total energy demand by nominally ~80%. How that simplifies things is that, ironically, producer services don't even record their energy uses. So you can only estimate them by the amount of money they are paid, and absent other information need to consider their energy impact to be "about average". That hugely simplifies everything, but takes a while to understand, starting with how the global average energy/$ is a very stable ratio, and can be known fairly precisely.

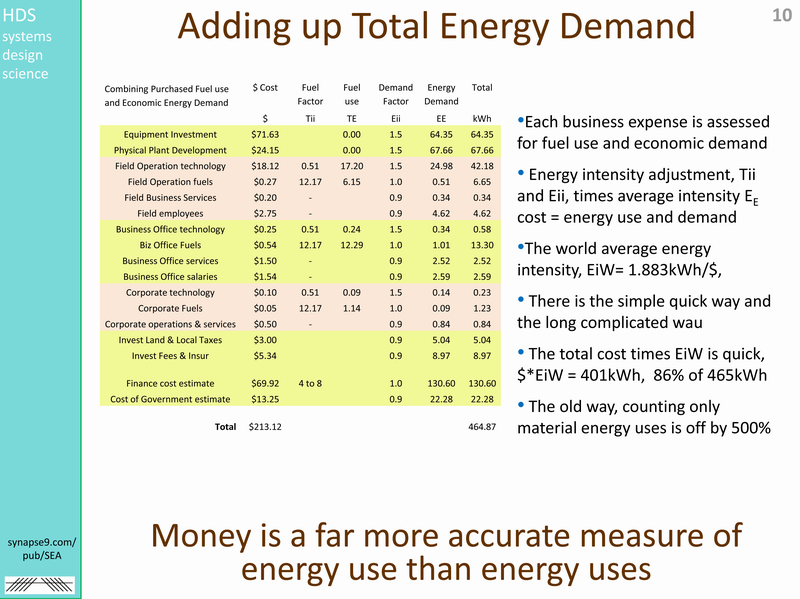

The Systems Energy Assessment (SEA) research paper shows that when you go to a great deal of effort to combine both ways of measuring, the exact accounting of the standard method is off by 500% and the quick method, using 8000btu/$, is only off by 15%. That using average spending habits rather than searching for records of energy uses FAR more accurate.

For example, a business will count the economic benefit of expanding the community that gives them development credits, causing the increased housing, commerce, infrastructure and services that the income to the community generates. Those large energy and other environmental impacts are all counted as business development benefits, but not counted for government environmental monitoring, using standards like the GHG protocol or the common measurement method LCA. I'd be interested in what anyone thinks.

2) To the UN Global Compact organization and appropriate staff - 6/13/11 http://www.unglobalcompact.org/AboutTheGC/contact_us.html

Deputy Director Power,

I’m a research scientist who has spent 30 years developing methods for describing and predicting the physical behavior of complex environmental systems. I’ve made some good progress too, but it is not being well utilized. The proofs are not so hard, just the unexpected questions that disregard popular myths, that then become quite simple for anyone to answer.

Because of what old myths fall away it’s kind of unpopular. Because we live in a natural world, though, it will have both technical and legal implications, that people will try to avoid , but eventually won’t be able to. I’d be delighted to follow up with your research staff. It could be quite important.

One of my recent findings concerns a flaw in our method for business energy and resource use accounting. Simply said, the standard method counts the traceable energy uses businesses pay for, often ~20% of the costs of running businesses. However, 100% of the costs of running businesses are ultimately traceable to the end user consumption of people at the ends of every supply chain, being paid for their services as a cost of operations. Most of those energy and other resource uses, then, are not counted by the ISO14000 and LCA application standard. For common types of businesses it causes an ~80% undercount of resource use.

I developed a sound method for correcting the problem, to be published in a pending special issue on resource accounting in Sustainability (MDPI). The paper is called, System Energy Assessment (SEA) and you can find my copy and a collection of supporting Slides & notes on my website. A pre-publication version is also in the Cornell physics archive arXiv:1104.3570v1 . It’s been a couple years since I figured out the problem. Everyone that looks at it has always agreed the method is valid too. The various professions it applies to are avoiding all effort to use of the new terms of discussion implied, however. It seems only if I was politically powerful would academics feel a need to change their work to reflect a better view of reality. Mother isn’t like that, of course, as everyone not being self-interested knows without hesitation.

How it effects the “precautionary principle” is that the error makes it possible to claim one thing and do the opposite regarding business resource demand. So much of the outsourced energy and resource uses of business are not counted that just outsourcing more appears to be a reduction when it is the reverse.

Thanks for all you and your organization’s work. We need the earth to work, not just our theories.

© Slides (click to enlarge) please use with attribution

)

)

)

)

)

)

)

)

)

)